In an effort to reduce emissions and align with the government’s Climate Action Plan 2021, significant changes to the Benefit-in-Kind (BIK) rules for company vehicles will take effect from January 1, 2023.

Both employers and employees may face increased costs for vehicles with higher CO2 emissions, and companies should review the vehicles provided to their employees in light of these changes.

Previously, the BIK cash equivalent for employer-provided cars was calculated based on the vehicle’s Original Market Value (OMV) and the employee’s annual business mileage.

Effect on the Company cars

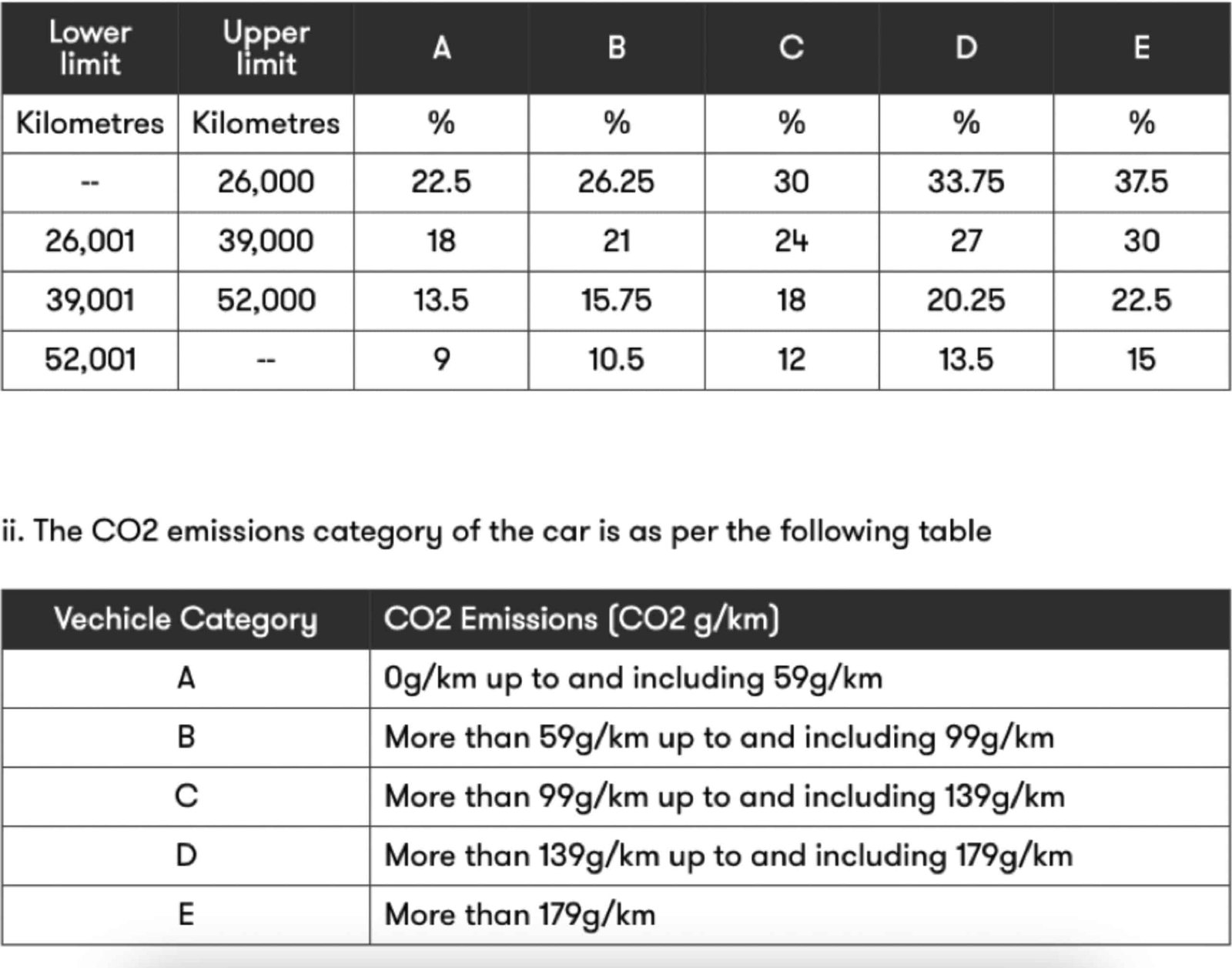

From 2023 onwards, the BIK cash equivalent will be determined using both the business mileage and the vehicle’s CO2 emissions. Vehicles will be placed into categories based on their CO2 emissions, and BIK rates will vary depending on the vehicle category and mileage.

The amount of business mileage and CO2 emission category

For example, On January 1, 2023, an employee receives a company car from their employer with an Original Market Value (OMV) of €28,000.

According to the manufacturer, the car emits 85g/km of CO₂. The employee drives 41,000 business kilometres during the year, placing the car in Vehicle Category B due to its CO₂ emissions.

With 41,000 kilometres driven in the year, the cash equivalent equals the OMV multiplied by 15.75% (for mileage between 39,001 and 52,000).

BIK Calculation: Cash Equivalent (OMV) €28,000 x 15.75% = €4,410

Comparing this to the current rules, if an employee drives 41,000 business kilometres and the car’s OMV is €28,000, the BIK calculation would be:

€28,000 x 12% = €3,360

Employers must keep records of the kilometres driven by each employee. It is recommended that these records be maintained on a weekly or monthly basis to facilitate accurate BIK calculations, which should be reported in real-time via weekly or monthly payroll returns. To ensure the BIK reported to Revenue is as precise as possible, employers are advised to review these records regularly, at least quarterly.

Also Read: Entrepreneur Relief Ireland – A Detailed Guide 2023

For Electric Vehicles

For electric vehicles (EVs), the government is phasing out the 0% BIK rate over the next four years.

However, tapered relief will apply to EVs made available for private use by employees from 2023 to 2025, with the OMV reduced by

€35,000 in 2023,

€20,000 in 2024,

€10,000 in 2025.

If the reduction reduces the OMV to Nil, a BIK charge will not arise. Any portion of OMV remaining, after the reduction is applied, is chargeable to benefit-in-kind at the prescribed rates.

For example, On January 1, 2023, an employee is provided with an electric company car with an Original Market Value (OMV) of €70,000.

According to the manufacturer, the car emits 50g/km of CO₂. The employee drives 24,000 business kilometres during the year, classifying the car as a Vehicle Category A due to its CO₂ emissions.

As electric cars will generally be categorized as ‘Category A’ vehicles, they will have CO2 emissions ranging from 0g/km to 59g/km inclusive.

The following examples demonstrate the impact of tapering relief and changes in BIK charges for employees over the next four years:

Section 118 (5H) TCA 1997 provides that from 1 January 2018 any expense incurred by an employer in the provision of electric vehicle charging facilities for employees and directors on the employer’s business premises, once all employees and directors can avail of the facility are exempt from the charge to BIK.

Also Read: 20 Tax Saving Opportunities for Businesses in Ireland

Employer Provided Vans

The cash equivalent for employer-provided vans will increase from 5% to 8% of the OMV starting in 2023.

Employers are required to maintain records of employee mileage and report BIK on a real-time basis via weekly or monthly payroll returns.

Revenue advises employers to review their BIK calculations regularly, at least quarterly, to ensure accuracy.

In conclusion, these changes to the company vehicle BIK rules will affect both employers and employees, and companies should review their vehicle policies and consider how these changes may impact their workforce and financial outcomes.

Need an Accountant in Ireland? Contact us now